Islamic banking in Bangladesh has become a strong and fast-growing sector since its launch in 1983. Currently, more than 10 full-fledged Islamic banks are operating in the country and several conventional banks are providing Shariah-based services through Islamic window or branch. According to Bangladesh Bank’s recent data, the Islamic banking sector is holding approximately 30% of the country’s total banking sector, indicating significant growth than before. This sector is expanding rapidly in both deposits and investment, and its popularity is increasing due to improving customer confidence and digital banking services.

DDM, FCFE, Residual Income and Relative Valuation methods used in the study based on the period 2017–2021 are still effective, but some changes are being observed in the current market situation. Although many Islamic banks are still considered somewhat overvalued, their future growth is strong due to increased competition, launching new services and improving technology-based banking systems.

Recent Information of Bangladesh Islamic Banking

Although Islamic banking in Bangladesh started its journey in 1983, the sector has become much more extensive and influential.

- Currently, more than 10 full-fledged Islamic banks and several conventional banks are operating in Bangladesh.

- According to the latest data, Bangladesh Bank report shows that the Islamic banking sector is now holding assets around 30% of the total banking sector (updated as of 2023-2024).

- In both cases, the growth of Islamic banks is faster than the traditional banks.

- The number of customers, branches and digital banking services have significantly increased.

Objectives of the Study

General Objective:

The main purpose of this study is to analyze the value of Islamic banking in Bangladesh, i.e., determining the real financial value and location of Shariah-based banks.

Specific Objectives:

This study presents the overall status of the Islamic banking sector, assessing performance and intrinsic value of banks, determining overvalued or undervalued position and comparing calculated and real intrinsic value.

Methodology of the Term Paper

This report is composed of theoretical analysis and quantitative methods. Analysis using different valuation models, which have been discussed in detail in the next chapters.

Data Source

For this study, secondary data has been mainly used. Reports published by banks as a source of information, previous research, news reports and related articles have been used.

Sample Size and Period

The study has taken data from 7 banks out of 10 Islamic banks in total. Five years of financial data analysis was used from 2020 to 2025.

Variables

This study has used various important financial indicators, such as: Risk-free rate, Market Return, Beta, Capital Asset Pricing Model (CAPM), Weighted Average Cost of Capital (WACC), Terminal Growth Rate, Share Price, Number of Shares Outstanding, Residual Income, Book Value per Share (EPS) and Price-Earnings (P/E Ratio).

Scope of the Study

This study has tried to determine the actual price of Islamic banking sector in Bangladesh. It will provide important instruction for investors and analysts, such as analysis of the growth of the sector, fair price (fair value), performance and relations with various economic elements.

Limitations of the Report

Like every study, this report has some limitations. Lack of experience during research management, lack of adequate information in some banks and completely dependence on secondary data has served as significant limitations. Besides, this analysis is based only on the application of different valuation models, it has not been provided directly with any policy recommendations.

- Research had limitations

- Some banks have not received enough information

- Analysis is entirely dependent on secondary data

- Only valuation model has been applied, no direct recommendation has been made

- Results may vary due to high volatility of capital market

- Big change in economic situation can impact research results

- Results should not be considered final, but exploratory

👉 Despite these limitations, a quality report has been attempted to prepare based on the information received.

Valuation Analysis and Findings

Valuation Analysis

The results of various valuation models used in this chapter are presented and the analysis from there. Here, as well as determining the intrinsic value of banks, the potential target price for the next 6 months based on forecast and market information.

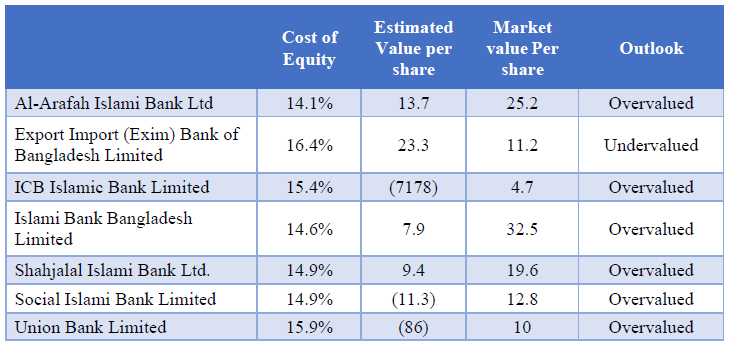

Dividend Discount Model (DDM)

According to Dividend Discount Model (DDM), ICB Islamic Bank Bangladesh Ltd. Without enough income, the dividend cannot be provided according to the rules. On the other hand, most banks have been evaluated as overvalued according to this model.

Free Cash Flow to Equity Model (FCFE)

The Free Cash Flow to Equity (FCFE) model is somewhat complicated to apply to the bank, because it is difficult to determine the bank’s net capital expenditure and non-cash working capital properly. That’s why the relevance of this model is relatively low and it doesn’t work properly in all cases.

However, an estimated calculation of the possible cash flow of the bank’s equity for the next 6 months is being considered differently.

According to Free Cash Flow to Equity (FCFE), cash flow to equity is the amount of money that is left for investors after the payment of debt and the reinvestment required in regulatory capital. The results of this account are presented at the table below.

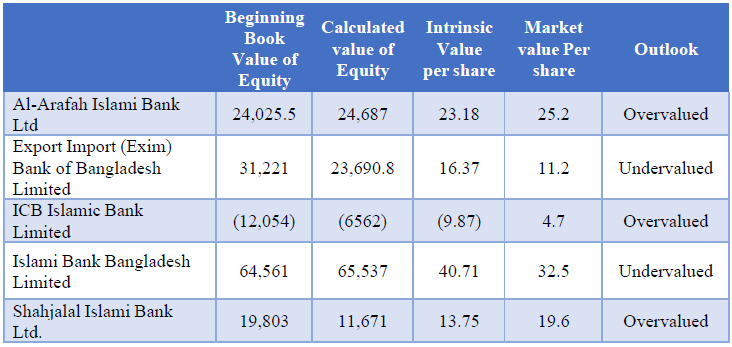

Residual Income Valuation

According to Residual Income Valuation, the total value of the terminal value and additional equity (surplus equity) decreases after converting the present value (value) to the value of the total value (value reduction occurs). The values of equity are presented in BDT million units.

The model’s account and structure are shown in Appendix. A target price for 7 banks has been set for the next 6 months. Analysis shows that Al-Arafah Islami Bank Limited, ICB Islamic Bank Bangladesh Ltd., Shahjalal Islami Bank Limited, Social Islami Bank Limited and Union Bank Limited—the most common targets for banks in these banks, where the fall of ICB Islamic Bank Bangladesh Ltd.

Conclusion

The study found that although most banks overvalued, the Export Import Bank of Bangladesh Limited (EXIM Bank) is mostly undervalued, which makes it the most likely in terms of future investment and indicates development opportunities.

In addition, the Social Islami Bank Limited, Al-Arafah Islami Bank Limited and Islami Bank Bangladesh Limited residual income value and peer-to-peer value are undervalued, indicating the possibility of improving the favorable economic environment.

The next 6 months’ price estimates show that the share price of the Export Import Bank of Bangladesh Limited (EXIM Bank) and Islami Bank Bangladesh Limited is likely to increase in the market. On the other hand, Al-Arafah Islami Bank Limited is in a relatively stable position, but other banks are in a slightly risky position. ICB Islamic Bank Bangladesh Ltd. The riskiest position is, whose performance reduction and the downward trend of share price has been noted.

Frequently Asked Questions

- Q1: What is Islamic banking?

- Ans: Shariah-based banking system where interest (interest) is banned.

- Q2: How many Islamic banks are there in Bangladesh?

- Ans: There are currently more than 10 full Islamic banks.

- Q3: How does Islamic Bank earn?

- Ans: Profit through sharing and business investment.

- Q4: How is bank valuation done?

- Ans: With DDM, FCFE, Residual Income and Relative Valuation Models.

- Q5: Which bank is more likely?

- Ans: EXIM Bank and Islami Bank Bangladesh are relatively more likely.